All You Need to Know About An Non-Resident (NR) Account

Ashish Jha

Co-Founder

Dec 19, 2024

Introduction

As an Indian living abroad, your financial life stretches across borders. From earning in one currency to maintaining commitments in another, the balancing act can often be complex. Whether you’re sending money to your family, saving for the future, or exploring investment opportunities in India’s rapidly growing economy, the right tools make all the difference.

Once you become an NRI, your regular resident Indian bank account becomes inactive as per regulations. You’ll need to convert it into an NRI-specific account to continue managing your finances legally and seamlessly. This is where a Non-Resident (NR) account steps in as a strategic solution. Beyond just banking, it becomes your bridge to India—a secure, efficient, and tax-smart way to manage your finances across geographies. An NR account not only simplifies the logistics of money management but also provides the flexibility and advantages that are crucial in today’s global economy.

Before we dive into understanding more, let’s get some basics right.

NR account

An NR account, or Non-Resident account, is a special type of bank account created to help Indians living abroad (called NRIs or Non-Resident Indians) manage their money in India easily. Imagine you’ve moved to another country—say, the US—for work or studies, but you still have ties to India. Maybe you own property here, have family to support, or want to save and invest in India. That’s where an NR account comes in.

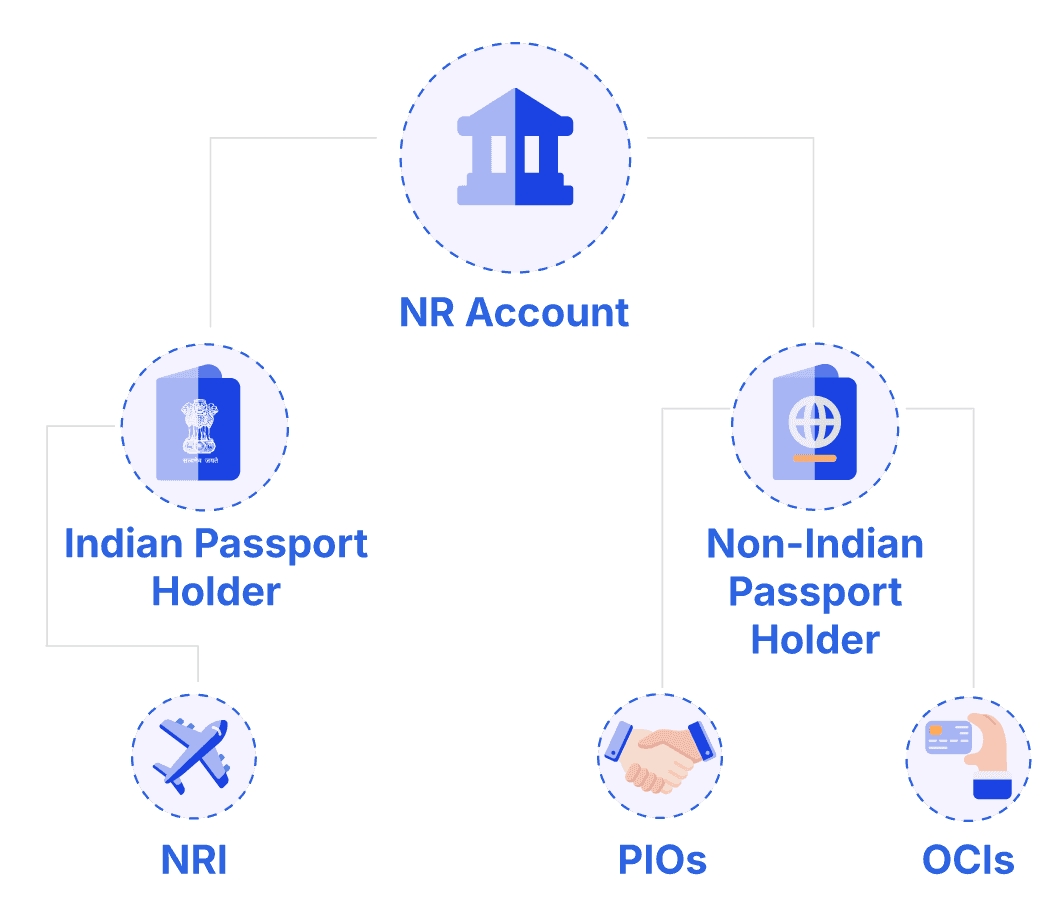

Who is eligible for an NR account?

The moment you get a gist on what an NR account is, the next question that arises is, how do you know whether you are eligible to get an NR account or not? Let’s understand the eligibility criteria for an NR account:

An NR Account is intended for individuals who meet the criteria of being a Non-Resident Indian (NRI) or a related category. Here's who is eligible:

Non-Resident Indians (NRIs):

'Non-resident Indian' is an individual who is a citizen of India or a person of Indian origin and who is not a resident of India. Thus, in order to determine whether an Individual is a non-resident Indian or not, his/her residential status is required to be determined under Section 6. As per section 6 of the Income-tax Act, an individual is said to be non-resident in India if he is not a resident in India and an individual is deemed to be resident in India in any previous year if he satisfies any of the following conditions:

If he/she is in India for a period of 182 days or more during the previous year; or

If he/she is in India for a period of 60 days or more during the previous year and 365 days or more during 4 years immediately preceding the previous year.

However, in respect of an Indian citizen and a person of Indian origin who visits India during the year, the period of 60 days as mentioned in (2) above shall be substituted with 182 days. The similar concession is provided to the Indian citizen who leaves India in any previous year as a crew member or for the purpose of employment outside India.

Persons of Indian Origin (PIOs):

Individuals of Indian ancestry but hold foreign citizenship.

Typically, PIOs are descendants of Indian nationals, up to four generations removed.

Overseas Citizens of India (OCIs):

Foreign nationals who have been granted OCI status by the Government of India.

OCI cardholders enjoy benefits similar to NRIs for holding bank accounts in India.

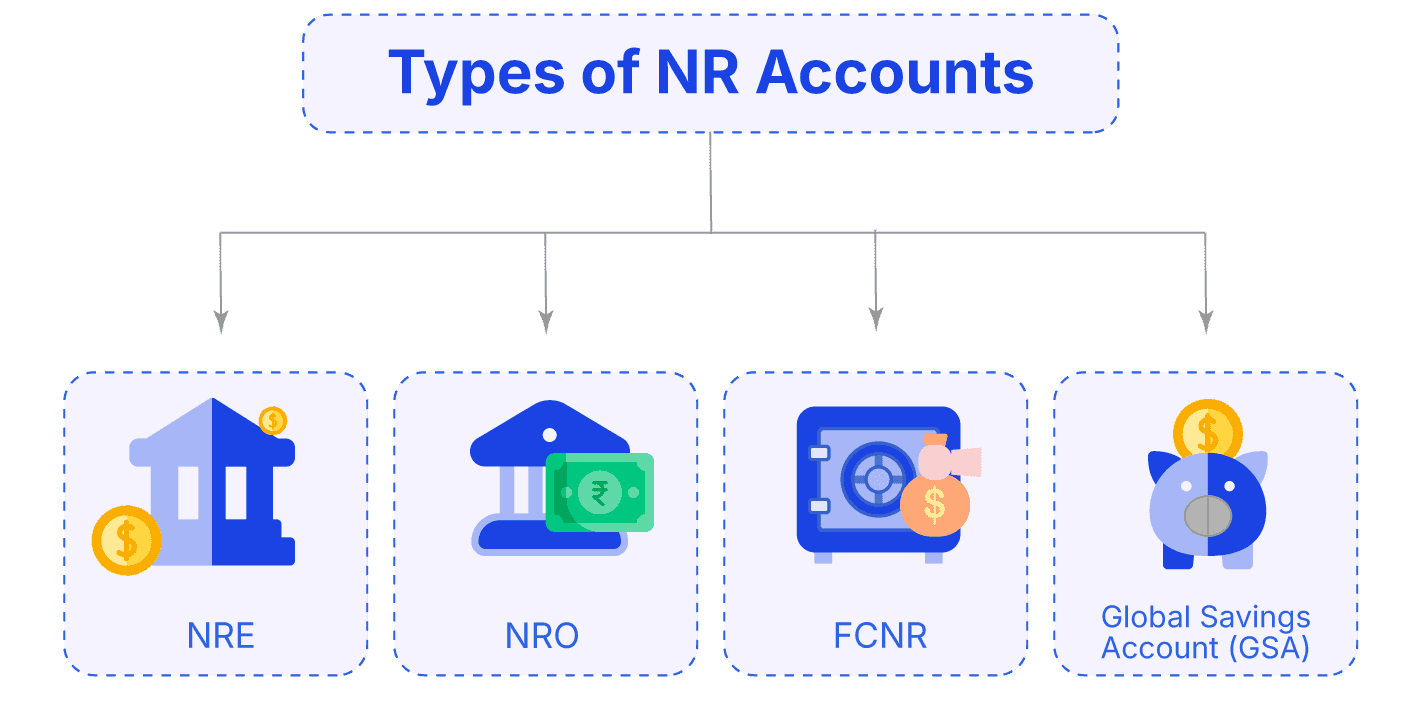

Types of NR Accounts:

Different types of NR accounts exist to meet the varied financial needs of Non-Resident Indians (NRIs). Savings accounts like NRE and NRO are designed for managing income from abroad and within India, respectively, with specific tax benefits and repatriation rules. Similarly, NRE FDs, NRO FDs, and FCNR FDs cater to different savings preferences, offering tax-free interest or protection against currency fluctuations. The introduction of the Global Savings Account (GSA) now allows NRIs to directly hold and manage foreign currency in their savings, offering more flexibility and ease in handling international funds. These options ensure that NRIs can efficiently manage their finances across borders.

To learn more in detail about each account type and how it fits your needs, keep scrolling!

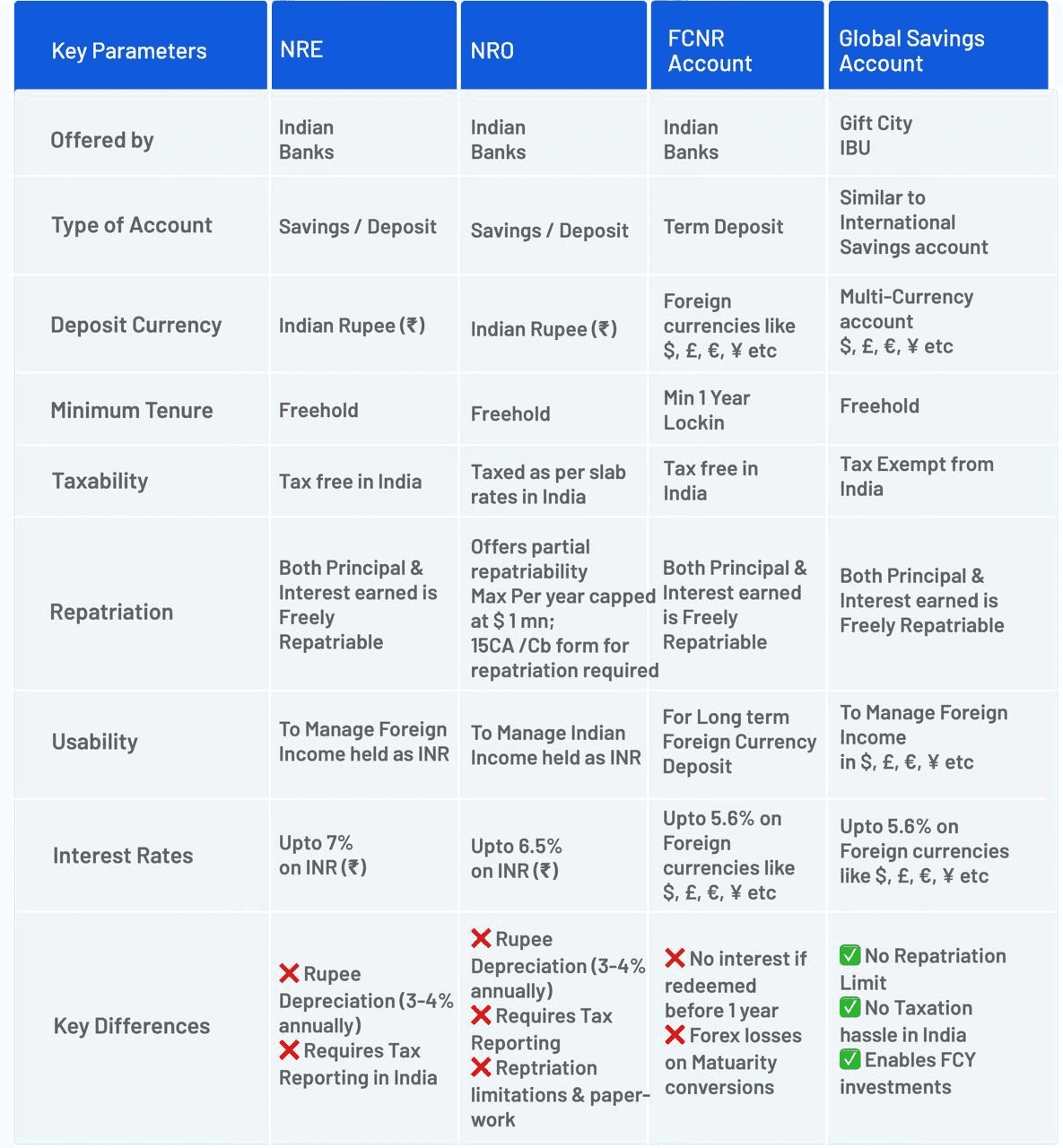

NRE Account (Non-Resident External Account):

NRE is like a foreign INR account. You can receive funds into this account from overseas. You don't pay taxes on interest and you can freely move money from here to overseas with no questions asked. You can also pay anyone in India from this account and use a debit card.

Used to park foreign earnings in India.

Funds are fully repatriable, meaning you can transfer them back to your foreign account without any restrictions.

Both principal and interest are tax-free in India.

Can be opened as a savings, current, or fixed deposit account.

NRO Account (Non-Resident Ordinary Account):

NRO is like any other local Indian account for non residents.You can move money to and from it into other Indian rupee accounts. You can have a debit card and use it to pay in India.

You pay taxes on interest earned on that account. If you transfer funds from this account to overseas, then you have to follow the regulations like max XXX per year, show document evidence of source of funds, tax clearance, etc.

Used to manage income earned in India, such as rent, dividends, or pensions.

Repatriation of funds is restricted to a maximum limit of USD 1 million per financial year (subject to RBI regulations).

Interest earned is subject to tax in India.

Can also be opened as a savings, current, or fixed deposit account.

FCNR Account (Foreign Currency Non-Resident Account):

Ideal for NRIs looking to save in foreign currencies while focussing less on exchange rate risks. This account helps preserve the value of your foreign earnings and offers tax-free interest in India, making it a secure and efficient way to grow your wealth internationally.

Allows NRIs to save their earnings in foreign currencies like USD, GBP, EUR, etc.

Protects against exchange rate fluctuations.

Interest earned is tax-free in India.

Typically opened as a fixed deposit account for a term ranging from 1 to 5 years.

Global Savings Account (Gift City):

For the first time in India, NRIs can now open a Savings Account which allows them to hold multiple currencies (upto 14+ currencies ).

These accounts are tailored especially for NRIs to manage foreign earnings with maximum flexibility. It combines tax exemptions in India with attractive returns on foreign currencies, allowing easy global financial management and investments.

Know more on Gift City IBU (Full form) Here

A multi-currency account offered through Gift City IBU, similar to an international savings account.

Designed to manage foreign income in currencies like USD, GBP, EUR, and JPY.

Offers up to 5.6% returns on foreign currencies while being completely tax-exempt in India.

Both the principal and interest earned are freely repatriable, with no repatriation limits.

Facilitates foreign currency investments (FCY) with ease.

Key Benefits:

✅ No taxation hassles in India.

✅ Freely move funds between countries.

✅ Manage savings or investments in multiple foreign currencies.

Benefits of using an NR Account

1. Managing Money across borders

If you’re an NRI (Non-Resident Indian) earning overseas, an NR account is your financial bridge to India. Beyond simplifying fund transfers, these accounts integrate with modern conveniences like UPI, allowing you to make quick payments and transactions back home—even from thousands of miles away. Whether you’re managing investments, paying bills, or supporting family, the ease of accessing and operating your account digitally ensures that staying connected to your finances in India is effortless and efficient.

2. Enjoy Tax-Free Savings

Who doesn’t like earning a little extra without the taxman taking a cut? If your goal is to grow your foreign earnings in India, an NRE (Non-Resident External) account is a top choice. The interest earned on your deposits, as well as the principal amount, is completely tax-free in India. This makes it ideal for NRIs looking to save or invest without worrying about tax deductions, helping their money grow faster.

However, it’s important to understand that an NRE account is designed exclusively for foreign income and cannot accept local deposits (such as payments from resident accounts in India). If you have income sources within India—like rent, dividends, or pension—you’ll need an NRO (Non-Resident Ordinary) account. While NRO accounts are subject to Indian taxes, they are better suited for managing day-to-day expenses and local transactions.

By choosing the right account—NRE for tax-free foreign savings or NRO for local income management—you can ensure your finances are both efficient and compliant with Indian regulations.

3. Effortless Transfer of Money Abroad (Repatriation)

Repatriation refers to transferring money from one country to another, and understanding how it works is crucial for NRIs managing international finances. If you’re earning abroad and want to transfer funds back to your country of residence, an NRE (Non-Resident External) account offers easy repatriation. Both the money you deposit and the interest earned can be sent abroad without any restrictions, making it an excellent choice for managing foreign income.

However, when it comes to NRO (Non-Resident Ordinary) accounts, repatriation is slightly more regulated. While you can transfer up to $1 million (or equivalent) per financial year from an NRO account, it requires additional documentation such as a certificate from a chartered accountant to ensure compliance with Indian tax regulations.

By choosing the right account based on your financial needs—unrestricted international transfers with NRE or regulated repatriation for local income with NRO—you can manage your finances effectively across borders.

4. Investing in India Made Easy

India offers a wealth of investment opportunities, from stocks and mutual funds to fixed deposits. With an NRE (Non-Resident External) account, you can invest in these options using your foreign earnings, providing a tax-efficient way to grow your wealth in India. On the other hand, if you have income sources within India, such as rent from property or pension payments, an NRO (Non-Resident Ordinary) account is better suited for managing those funds.

While NRE accounts are ideal for handling your overseas earnings and enabling tax-free repatriation, NRO accounts are designed for managing local income and expenses, ensuring effortless financial management within India. Both accounts cater to different financial needs, making it easy for NRIs to stay connected with India’s growing economy.

5. Meet Financial Obligations Back Home

Life in India doesn’t stop just because you’ve moved abroad. Whether it’s paying your parents’ medical bills, managing household expenses, or even contributing to family celebrations, an NR account ensures you stay connected to your financial responsibilities back home.

For instance, you can easily use an NR account to pay utility bills like electricity and water, settle property maintenance charges, or handle EMIs for loans you’ve taken in India. During your visits to India, these accounts simplify managing everyday expenses—be it dining out, shopping, or gifting.

With the use of UPI, managing these payments becomes even faster. Imagine using UPI to instantly transfer funds or pay vendors directly from your NR account, just as conveniently as if you were in India. From covering day-to-day needs to planning for long-term goals like saving for your retirement, an NR account equips you to handle it all effortlessly.

6. Easily Support Your Family Back Home

Being away from your loved ones doesn’t mean they can’t access the funds they need. With the UPI Circle feature, you can ensure that your family members in India have access to your funds when required.

By linking your NRE or NRO account to UPI, you can authorize them to make payments or withdrawals directly from your account, without the need for you to be physically present. This provides a convenient and secure way to manage family expenses, offering a reliable safety net for both emergencies and day-to-day needs.

Get NRE / NRO account with Rupeeflo

Click here to download the App.

UPI for NRIs

If you’ve been away from India for a few years, it’s time to catch up on how UPI has transformed the payment landscape.

What is UPI?

UPI (Unified Payments Interface) is a real-time payment system developed by the National Payments Corporation of India (NPCI), designed to make digital transactions simple, fast, and secure. It allows users to transfer money instantly between bank accounts using a mobile phone without requiring account details like IFSC codes or account numbers.

UPI has become India’s backbone for digital payments, processing over 10 billion transactions monthly worth more than ₹15 trillion. It powers payments across urban and rural areas, with over 50 million merchants accepting UPI. Its ease of use and features like QR payments, UPI Autopay, and global integration make it the go-to platform for everything from groceries to online shopping.

UPI’s impact goes beyond convenience—it’s driving financial inclusion and making India a global leader in digital payments.

What is UPI Circle?

Now you can allow your parent or your family member to make payments from your UPI account while you maintain the control or access.

This exceptional feature allows you to link your bank account to the UPI (Unified Payments Interface) system and grant authorized family members or trusted individuals access to make payments or transfers on your behalf. It’s a secure and convenient way for your loved ones to access funds directly, eliminating the need for your physical presence or additional documentation.

Whether it’s paying household bills, managing medical expenses, or covering urgent payments, this feature offers much-needed flexibility to manage your finances in India, even when you’re abroad. It’s the perfect solution to ensure your financial responsibilities are handled effortlessly, anytime and anywhere.

How can an NRI access UPI?

UPI Access with International Numbers

NRIs can now link their Indian bank accounts to UPI using their international mobile numbers. This means you can enjoy instant payments in India without the need for an Indian number. Pay for family expenses, shop during your visits, or transfer funds—all with the same ease as locals.

Why Should NRIs Use UPI?

Simplified Transactions: No need for cash or card hassles during India visits.

Quick Payments: Instantly pay bills, send money to family, or donate to causes.

Global Integration: A convenient way to manage your Indian finances from abroad.

Embrace UPI and stay financially connected to India effortlessly!

Steps to get UPI with your international number

Use Case 1: If You Already Have an NRE/NRO Account

If you're an NRI with an NRE or NRO account, you can link your international mobile number to UPI and enjoy seamless transactions. Here's how:

Ensure Your International Mobile Number is Registered with Your Bank:

Contact your bank to confirm that your international mobile number is linked to your NRE or NRO account. This is crucial for UPI activation.

Choose a UPI-Compatible Application:

Select a UPI application that supports international mobile numbers. Banks like ICICI Bank offer the iMobile Pay app, which facilitates UPI transactions for NRIs.

Register on the UPI Application:

Download and install the chosen UPI app.

Initiate the registration process by verifying your international mobile number.

Link your NRE or NRO account to the UPI app as per the app's instructions.

Create a UPI ID and Set a PIN:

Follow the app's prompts to create a unique UPI ID.

Set a secure UPI PIN to authorize transactions.

Start Transacting:

With setup complete, you can now send and receive payments using UPI. This includes paying Indian merchants, transferring funds to Indian bank accounts, and scanning Indian QR codes for payments.

By following these steps, NRIs with NRE or NRO accounts can leverage UPI's convenience for their financial transactions in India.

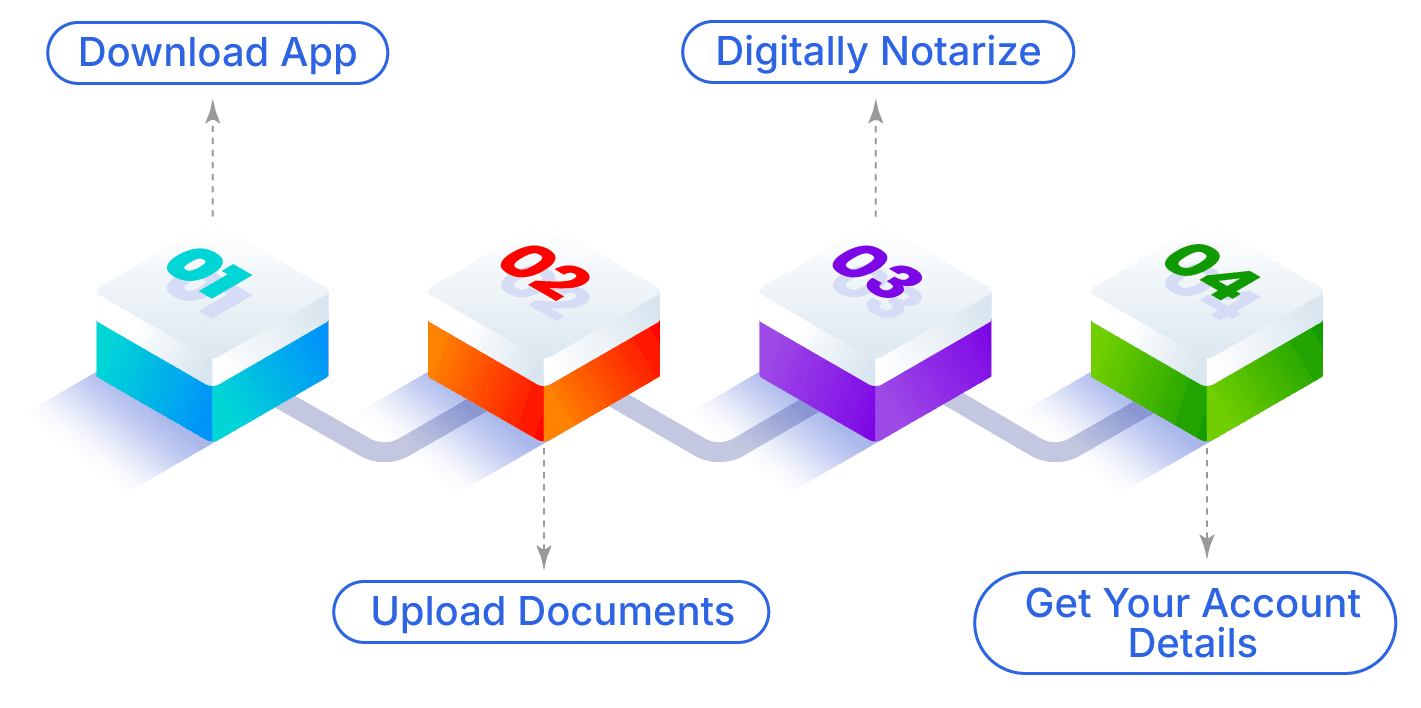

Use Case 2: If You Don’t Have an NRE/NRO Account (Process with Rupeeflo)

For NRIs without an NRE or NRO account, Rupeeflo simplifies account opening and access to UPI. Here’s a streamlined overview:

Step 1: Login and Application Submission

Download the Rupeeflo app, create an account, and submit the application.

Step 2: Document Upload

Upload required KYC documents:

For Indian Residents: PAN Card, Passport, Address Proof (not older than 3 months), Passport Photo, Signature, and proof of NRI status (e.g., Visa or Permanent Resident document, if applicable).

For International Users: SSN (US), National Insurance Number (UK), or NRIC (Singapore), along with a valid Passport.

Time: ~10 minutes

Step 3: Digital Notarization

Schedule an online notarization appointment via the app.

Present documents during a live video call with the notary for verification.

Notarized documents are uploaded directly to your app.

Step 4: Account Number Assignment

Account number is assigned within 24 hours of document submission.

In Conclusion

An NR account is more than just a way to manage money—it’s a lifeline that connects you to your financial commitments and opportunities in India. With benefits like tax-free savings, hassle-free fund transfers, and investment-friendly features, it’s a smart move for any NRI. Choose between an NRE and NRO account based on your needs and enjoy peace of mind knowing your finances are in order, no matter where you are in the world.